Investment #9: Thermal Energy International

Lean, green, growth machine

If you’ve read the first few posts you will be familiar with my skepticism of “tick-box”, first-level thinking, unrealistic and capital destructive approaches to ESG. However, ESG, like most real world issues, is not black and white but nuanced. Like almost everyone else, I want less pollution, more green spaces, cleaner water, less people in poverty now and better living conditions for our descendants. Where I disagree is how we get there.

Never before in human history have we deliberately moved into energy sources that are inherently orders of magnitude less efficient and less reliable. This can only be justified by an obsession with a single factor (e.g. point of use carbon emissions) and ignoring the reality of the value chain and massive negative externalities (e.g. mining, back-up power plants, grid issues, social costs, more poverty). So I have trouble with traditional “green” investments such as electric vehicles or renewable energy, which I think will eventually only form a small part of the solution.

What I really get excited about are companies and products that achieve these goals while creating value. This is not in the narrow sense, i.e. for shareholders via some regulatory arbitrage or with subsidies, but for the broader economy. These are the truly sustainable investments. Companies, individuals and the environment stand to benefit. It creates a virtuous circle.

On that note: Thermal Energy International (TMG). See the description and main catalysts below as per usual. The short pitch from me: TMG provides thermal energy efficiency solutions to the industrial sector, its the fastest and easiest way to reduce carbon emissions, it has quick pay-back and high ROI for customers, strong revenue growth and a huge runway ahead of it. It trades at C$0.28/market cap C$48mn and the CEO bought stock at a similar level in February.

I came across this idea from

, the famed micro and small cap investor. He has given details about this publicly in several places. The CEO has done several public interviews and there are further details on Micro Cap Club, Small Cap Discoveries, YouTube and a few podcasts.As a reminder this is primarily an investment journal, this is not financial advice or a recommendation. All of the ideas are plundered from other (cited) sources. I simply own the stock. Please refer to the disclaimer at the bottom or my introductory post for further details.

Ticker: TMG CN

Average entry price: ~C$0.26

Current price: C$0.28 (12-Mar-24)

Upside scenario: ~C$0.5-1 (+2-4x, 3 year horizon)

Position size: ~$10k

Thermal Energy International IR Presentation

Description

Thermal Energy International (TMG) is an international supplier of proprietary energy efficiency solutions primarily for industrial sites. TMG aim to significantly reduce industrial energy use, saving customers money and reducing carbon emissions. For a description of the main technologies see descriptions of GEM steam traps, FLU-ACE and DRY-REX.

Investment thesis and catalysts

The right business for the zeitgeist: “Energy efficiency is the fastest, cheapest and easiest way for companies to reduce carbon emissions… Unique proprietary solutions provide high ROI, with short compelling payback period”. Energy efficiency is the worlds “first fuel” with ~2/3rds lost. In order to meet net zero goals the IEA (for all my skepticism of them…) estimate investment in energy efficiency needs to triple to 2030. 90% of industrial energy use is thermal and 50% is lost as waste heat. This comes at a time where the cost of carbon in the EU has increased ~3x since 2019. TMG offer a series of solutions that can recover up to 80% of energy lost in a typical boiler plant. It offers turnkey solutions at a fixed price with guarantees around performance.

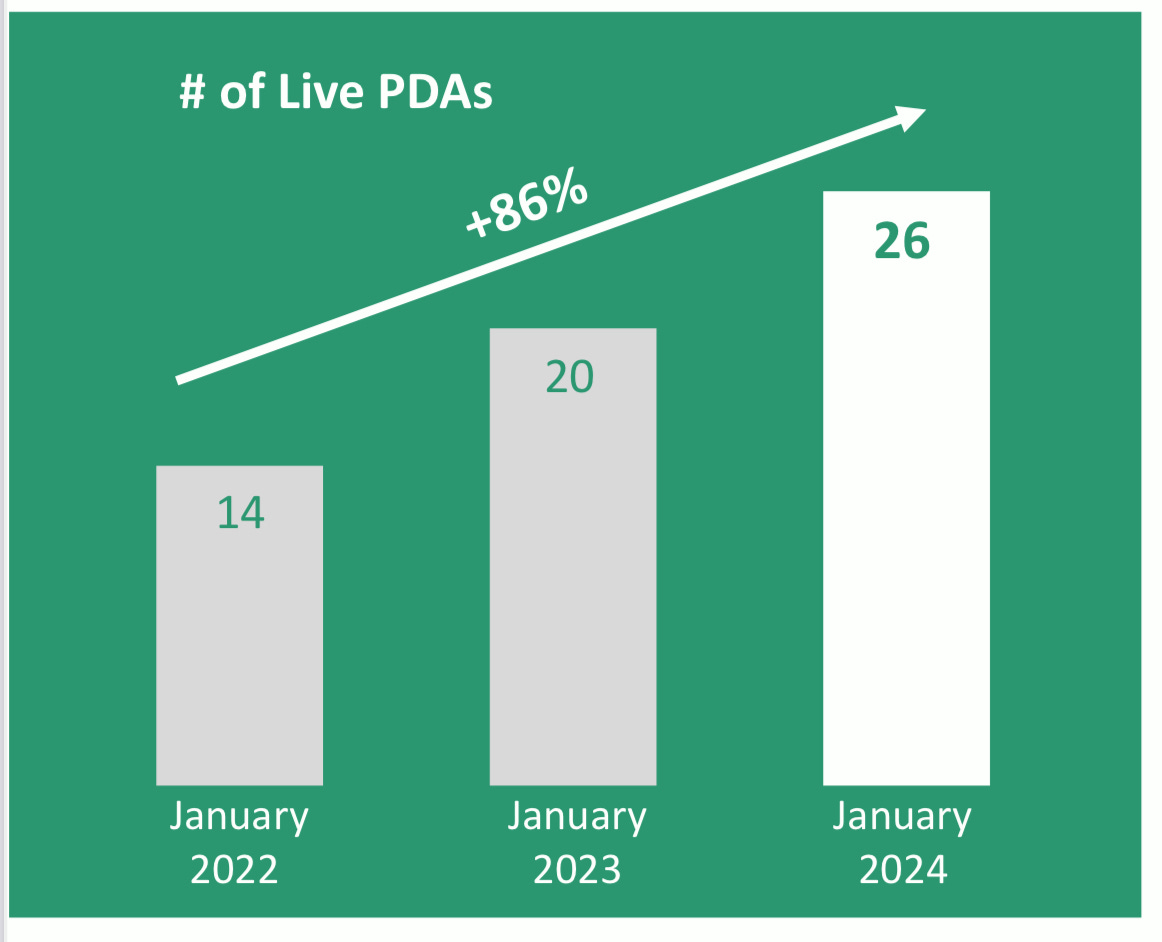

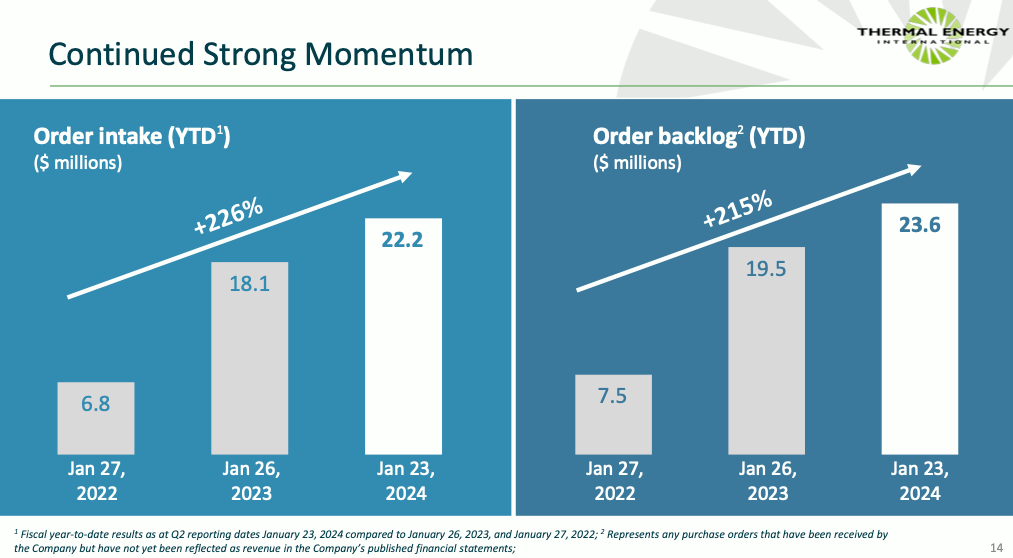

A strong track-record and extended runway: The pandemic was a large set-back for the business, but it is now beginning to motor again. It is probably worth splitting in pre-pandemic and pos pandemic. Pre-pandemic 5 years revenue growth was 30% CAGR. Various complementary acquisitions have offered significant advances in energy recovery. TMG benefits from a lot of repeat business, in the last 4 years 60% of orders have come from the top 10 customers. But there is still a long runway: TMG has only partially penetrated ~100 sites for these customers across 15 different countries, these customers have >1,000 sites worldwide. Project development agreements (PDAs) at 1H24 (FY May-end) were 300% higher than FY19. PDAs conversion into firm orders are around 75%. TMG averages $1-3mn per order. TMG is increasingly selling into corporate HQs instead of individual sites, this can add momentum with orders for multiple sites. From an end user perspective, TMG’s services work best when the site loses energy as heat somewhere but also could use the heat elsewhere close by. There are energy intensive sectors that have no use for the heat (i.e. steel, cement etc), which makes them less attractive customers. On the other hand food & beverage (use heat for heating, cook, clean, wash, package), pharmaceuticals, tyre manufacture, plastics, rubber, hospitals and universities are all target industries.

Limited competition. 90% of revenue is sole sourced with customer, in terms of turn-key projects with proprietary technology there are no real competitors. The alternative is some similar “next best” equipment but rarely is TMG competing directly with them. Customers would have to hire an engineering company to develop the project, source the equipment themselves and hire a contractor to install it. This is creates far more execution risk and longer lead times.

Aligned management: The main man is CEO Bill Crossland. He has actively purchased a lot of shares on the open market and now has ~5.7mn shares (check). The CEO bought more stock around C$0.27 in February. The vast majority of his stock has been bought with his own cash, as opposed to vested with options, better aligning him with shareholders. However total insider ownership is relatively low at only ~7.8%. Furthermore the total share count (169mn) is a bit large for micro cap investors that like a bit more torque.

Share buy-backs: TMG will generate a decent amount of cash while profitable. It is a virtual manufacturer with little cash tied up in equipment. It runs tight WC with turnkey projects helping cash flow. Debt pay-down is probably the first priority given a small amt. of still high cost debt ($2.8mn at 8.2%-13.3%). Beyond that TMG is likely to look at accretive M&A to expand distribution or product suite. Failing that share buybacks may be an option (as it did in very small size 2014-16).

Valuation still reasonable: TMG has a ~C$49mn EV with a very small net debt position. On a LTM basis the company is growing revenues by 55% y/y and EBITDA has gone from 0.9mn to 3.3mn for a ~15x EBITDA multiple. In terms of 2Q stand-alone - revenue grew 71% y/y. However, as per the estimates above with respect to the backlog, this still looks undemanding on a FY25 basis. If we conservatively assume growth next year moderates somewhat to ~50% y/y, I still get to ~C$36mn in revenues. Again if we conservatively assume EBITDA margins are relatively flat at ~12% ( reflecting return of some larger lower margin turn-key projects holding back operating leverage) I arrive at a 9x EBITDA multiple.

Risks

Slowing growth: Orders are lumpy and it’s not really a quarterly business. Temporary slow downs could impact the stock price.

Natural gas/energy prices: low energy costs can disincentivise customers to pursue these solutions. However demand is now more driven by carbon reduction goals. Cost per ton of carbon keeps increasing. Pay-back is usually 1-3 years, some consumer centric brands would settle for 9-10 years as pay-back is less relevant than carbon reduction.

Rowing back carbon pricing. Carbon pricing appears to be the main driver for companies to implement project. A regulatory about turn, while unlikely, could upend the demand case.

Competition: CEO says he gets in trouble for saying they “don’t really have competition”. It appears that no-one else has the same suite of products as well as turn-key execution. However this leaves the potential for someone to emerge.

Value destructive M&A: Management will seek bolt-on deals.

Credits, sources and where to find more

I came across this idea from

the famed micro and small cap investor. He has given details about this publicly in several places. The CEO has done several public interviews and there are further details on Micro Cap Club, Small Cap Discoveries, YouTube and a few podcasts. A link to the interview with Paul Andreola is here:Happy hunting,

The Geez